Why Has the King of Altcoins Found Itself Surrounded by Crisis?

Sep.19.2024

Author: YBB Capital Researcher Zeke

Preface

The halving rule is beginning to falter, and many altcoins are languishing. Speculators are leaving the scene, while believers are starting to doubt themselves. The despair in the industry stems not only from the price slump in the secondary market but also from uncertainty about the future direction. Criticism has become the main theme within the space, dissecting everything from the lack of applications to the minutiae of financial reports from major blockchains. Now, the spotlight is on what was once the fertile ground for crypto — Ethereum. So, what exactly is the internal struggle of the “king of altcoins”?

1.Horizontal Expansion of the Main Chain, Vertical Layering

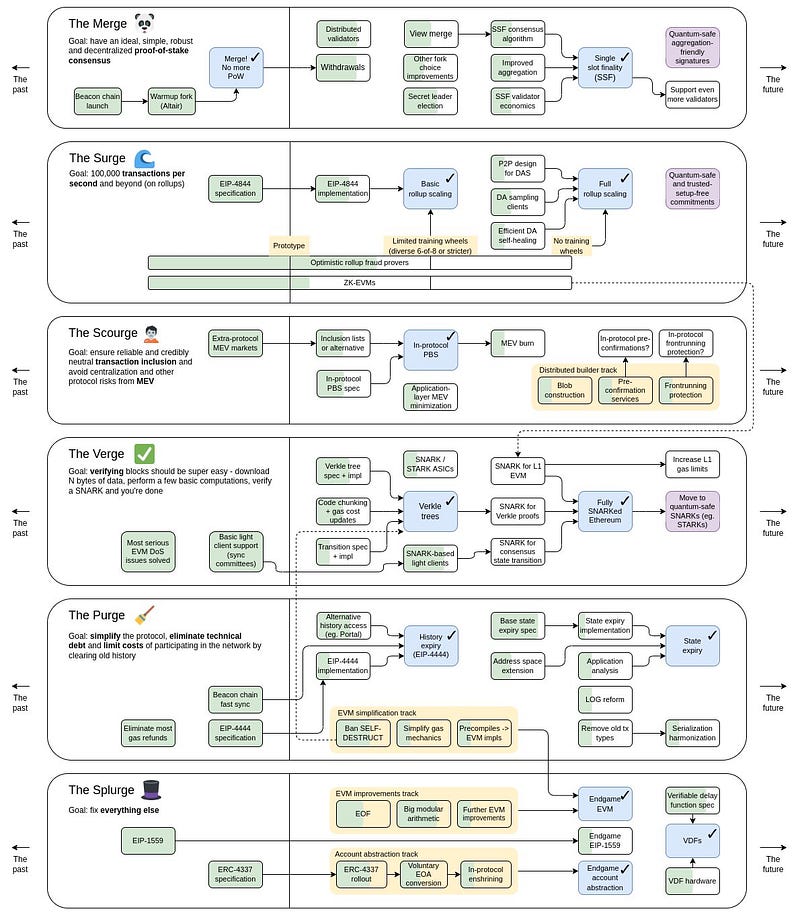

Vitalik’s vision of Ethereum’s endgame was set between 2018 and 2019: to achieve fractal scalability through complete modularization. The idea was to optimize the base layer around Data Availability, while infinitely scaling the upper layers, thus bypassing the blockchain trilemma and positioning Ethereum as the settlement layer for countless chains, ultimately reaching the endgame of blockchain scalability.

Once this vision’s feasibility was confirmed, Ethereum’s roadmap rapidly advanced in both horizontal and vertical dimensions. In 2023, with the successful merger of the main chain and Beacon Chain during the Shanghai upgrade, modularization became the driving theme of the Ethereum ecosystem. Now, with the Cancun upgrade taking the first steps toward EIP4844, the main chain is approaching Vitalik’s early vision. The upper layers are also flourishing, with improvements in Gas, TPS, and diversity steadily surpassing previous competitors. Aside from the issue of fragmentation, the narrative of Ethereum Killers from heterogeneous chains should now be considered over. But the harsh reality is that TON and Solana are rising, and many projects copying the modularization narrative are outperforming the “modularization pioneer” Ethereum in the secondary market — even with the ETF boost. What is the cause of this situation?

The transition to PoS and the development of Layer 2 have recently been the focal points of criticism against Ethereum. However, in my view, neither Vitalik nor the Ethereum developers have erred in advancing modularization. If there is a fault, it might be that this process has been pushed forward too quickly and too idealistically. In an article I wrote earlier this year, I mentioned something along these lines: if blockchain truly has significant use cases outside of the financial sector, and if mass adoption will eventually come, then Ethereum’s shift towards modularization makes sense. Clearly, Ethereum has been too idealistic in this regard, as there are currently no signs that these two conditions are being met. The same goes for the pricing curve of DA. Given the current state of Layer 2, the anticipated explosion of the application layer has not materialized. Moreover, many general-purpose chains have dwindled, with only ARB, OP, and Base remaining active. Revenue from DA alone is far from enough to sustain Ethereum’s positive cycle.

There are other lingering issues as well. For instance, Gas consumption has dropped by tens or even hundreds of times; what used to require 0.1 ETH now only needs 0.001 ETH, yet user activity has not increased by the same magnitude, leaving supply far greater than demand. Still, pushing public chains toward large-scale adoption while maintaining maximum decentralization and security doesn’t seem wrong. Ethereum has managed to turn much of its eight-year-old “promises” into reality, which is commendable in the crypto world. Unfortunately, the market is driven by pragmatism, not ideals. In the absence of applications and liquidity, the conflict between the idealism of Ethereum’s tech-driven ambitions and the demands of investors will continue to deepen.

2. Human Nature

Ethereum’s idealism is not only evident in its vision for the future of the application layer but also in its understanding of human nature. Currently, two of the most discussed issues regarding Layer 2 are: 1) centralized sequencers and 2) tokens. From a technical perspective, it is possible for Layer 2 to achieve decentralization. However, from the standpoint of human nature, it is highly unlikely that top Layer 2 projects would relinquish the immense profits generated by sequencers unless decentralization somehow boosts the value of their tokens and yields even greater benefits. For example, the leading Layer 2 projects certainly have the capability to decentralize their sequencers, but they choose not to. This is because they are top-down projects, fueled by massive funding, and their mode of operation is highly reminiscent of Web2. The relationship between community members and Layer 2 is more like that of consumers and a cloud service provider. Much like frequent users of Amazon’s AWS servers might receive discounts or cashback offers, Layer 2 projects offer airdrops. However, for Layer 2 projects, the revenue from sequencers is their lifeblood. Design, funding, development, operations, and hardware purchases do not require community support. In their view, users contribute very little, which explains the often indifferent attitude many Layer 2 projects have towards their users. Consequently, there is little chance of decentralizing sequencers, as merely appealing to a sense of ethics won’t suffice. To decentralize sequencers, a new design must align with the interests of Layer 2 project teams, but such a proposal would undoubtedly be controversial. The better approach might be to erase or indefinitely postpone any roadmap item related to decentralized sequencers. Presently, Layer 2 projects stand in direct opposition to Ethereum’s initial modularization goals; most of them merely shift concepts and siphon away anything valuable from Ethereum.

Let’s move on to tokens. Layer 2, in its current form, is still a relatively new concept in the crypto space, and tokens create significant contradictions when viewed from the perspectives of Ethereum, Layer 2 project teams, and the broader community. Let’s start with Ethereum’s viewpoint: from Ethereum’s perspective, Layer 2 should not issue tokens. Layer 2, in Ethereum’s ecosystem, is akin to a “high-performance scaling server” that is simply used across chains and charges service fees. For both Ethereum and Layer 2, this is a healthy model, as it maximizes the stability and value of ETH. In more tangible terms, if the entire Layer 2 ecosystem were compared to the European Union, maintaining the stability of the Euro is paramount. If many member states begin issuing their own currencies, weakening the Euro, the European Union and the Euro could ultimately collapse. Interestingly, Ethereum does not restrict Layer 2 from issuing tokens, nor does it mandate the use of ETH as gas fees. This open attitude toward rules is quintessentially “crypto.” However, as ETH continues to weaken, the “EU members” are showing signs of restlessness. In the primary tools used by top Layer 2 projects to issue new chains, it is clearly stated that projects can use any token for gas fees and choose any integrated DA (Data Availability) solution. Additionally, one-click chain issuance will likely lead to the formation of smaller alliances within the Layer 2 ecosystem.

Now, let’s look at things from the perspectives of Layer 2 and the community. Even if ETH stages a strong rebound in the future, tokens still face a dilemma. In fact, major Layer 2 projects were initially hesitant to issue tokens. Besides the opposition from Ethereum mentioned earlier, there are several reasons for this: regulatory risks, no need for additional funding due to sufficient capital, difficulties in determining the scope of token utility, and the fact that directly using ETH would more quickly drive TVL (Total Value Locked) and ecosystem growth. Issuing their own tokens could conflict with this goal, and liquidity would never surpass that of ETH.

Again, it comes down to human nature. Printing tens of billions of dollars out of thin air is something few can resist. Moreover, from the perspective of community members and ecosystem development, tokens seem necessary. In addition to collecting fixed service fees, they provide a treasury that can be cashed out at any time — what’s not to love? But the design of tokens must also take into account the aforementioned problems, leading to minimized utility. As a result, a slew of “air tokens” that neither require PoS staking nor PoW mining has emerged. These tokens serve one purpose: voting. Each time they are linearly released, they drain liquidity from the market. Over time, these tokens, lacking any real driving force, will continue to decline after an initial airdrop, leaving both the community and investors unsatisfied. So, should these tokens be empowered with utility? Any form of meaningful utility will contradict the issues discussed above, leading to a Catch-22 situation. The situation with the tokens of the “four kings” of Layer 2 perfectly illustrates these problems.

On the other hand, Base, which has not issued a token, is faring much better than Zks or Starknet. Its sequencer revenue has even surpassed that of Superchain creator OP. As mentioned in previous articles about the attention economy, leveraging social media influence, project operations, and price-pumping strategies to create wealth effects for MEME tokens and various projects is a form of indirect, multiple small airdrops. This approach is far healthier than directly issuing a token followed by a one-time airdrop. Besides continuously creating attraction, it avoids many problems. By allocating a portion of sequencer revenue each month, Layer 2 projects can maintain activity and build a sustainable ecosystem. It’s worth noting that the current point system in Web3 is merely a superficial imitation of PDD’s model. Coinbase’s steady, long-term operational strategies far surpass those of explosive players like Ironfish.

3. Malignant Competition

There is a growing trend of homogenization between Layer 1 and Layer 2, and even among different Layer 2 solutions. This situation stems from a critical issue: in this cycle, there are very few independent applications that can justify the existence of an application-specific chain, and the few that did manage to stand out have “run away” (such as DYDX). Currently, it can be said that all Layer 2 projects are targeting the same user base, even overlapping with Ethereum’s main chain. As a result, a very problematic phenomenon has emerged: Layer 2 solutions are constantly cannibalizing Ethereum, while simultaneously engaging in vicious competition among themselves for TVL. No one can clearly distinguish between these chains, and users rely on incentive programs to decide where to store their funds or which platform to trade on. Homogenization, fragmentation, and a lack of liquidity — Ethereum is currently the only public chain ecosystem that encapsulates all three of these issues simultaneously. These problems also arise from Ethereum’s inherently open spirit, which has led to some drawbacks. We may soon witness the natural elimination of many Layer 2 solutions, and the centralization problem will likely cause various forms of chaos.

4. The Leader Doesn’t Understand Web3

Whether it’s the earlier “Vitalik,” or today’s “Little V,” Vitalik Buterin’s contributions to infrastructure have undeniably driven the crypto space into a new era of prosperity, second only to Satoshi Nakamoto. However, the reason he is now referred to as “Little V” stems not only from issues in his personal life but also from a popular criticism: the Ethereum leader doesn’t understand DApps, and even less so DeFi. To some extent, I agree with this statement, but before delving into this topic, I want to clarify something: Vitalik is just Vitalik — neither an omnipotent god nor an incompetent dictator. In my view, Vitalik is a relatively humble and active leader in the blockchain space. If you’ve read his blog, you’ll notice that he regularly posts one to three updates on topics ranging from philosophy to politics, infrastructure, and DApps. He also enjoys sharing on Twitter. Unlike some blockchain leaders who occasionally lash out at Ethereum, Vitalik is much more pragmatic.

Now that I’ve said some positive things, let’s address the issues I see with Vitalik:

His influence on this space is too great — affecting everyone from retail investors to VCs. Every word he says impacts people’s decisions, and “To Vitalik” has become a pathological trend among Web3 project founders.

He is overly committed to certain technological directions he favors, to the point of endorsing them publicly.

He might not fully understand what crypto users truly need.

Let’s start with Ethereum’s scalability. The notion that Ethereum urgently needs to scale is often supported by the extraordinarily high on-chain activity from 2021 to 2022, driven by abundant external liquidity. But every time Vitalik discusses this topic, it seems he doesn’t realize this was a temporary phenomenon, and he misses the point of why users flocked to the chain in the first place. Another example is his repeated emphasis on the technical superiority of ZK (Zero-Knowledge) technology in Layer 2 solutions. However, ZK technology is not particularly user-friendly, nor is it conducive to ecosystem growth. Today, many ZK Rollup projects founded with the “To Vitalik” mindset are not just in the T2 or T3 category; even the top two players are struggling to survive, while the performance of the three giants of Optimistic Rollups surpasses that of all ZK Rollups combined. There are other similar issues, such as last year’s criticism of MPC (Multi-Party Computation) wallets, which was overly one-sided, favoring AA (Account Abstraction) wallets instead. Even earlier, he proposed the concept of Soulbound Tokens (SBT), but their practical applications turned out to be underwhelming, to the point where they are rarely mentioned anymore. In short, most of the technical solutions Vitalik has supported in recent years have not performed well in the market. Lastly, his recent comments on DeFi have also been perplexing. Taking all these factors into account, it’s clear that Vitalik is not perfect. He is an excellent developer with idealistic visions, but he lacks a deep understanding of the user base and sometimes makes subjective statements on topics he doesn’t fully grasp. The industry needs to demystify Vitalik and approach controversies surrounding him with clarity and discernment.

5. From Virtual to Real

From the ICO craze in 2016 to the P2E bubble in 2022, the blockchain industry has seen various Ponzi schemes and new narratives emerge in each era, driving the sector toward larger and larger bubbles, constrained only by infrastructure limitations. We are now witnessing the bursting of these bubbles — projects with massive funding are self-destructing, grand narratives are failing, and there is a growing disconnect between Bitcoin and altcoin value. The question of how to create real value has been a recurring theme in many of my articles this year. Moving from the virtual to the real world is also the current prevailing trend. While Ethereum embraces modularity, some have declared that the narrative of “Ethereum killers” has ended. Yet today, the hottest ecosystems are TON and Solana. Have these chains brought any innovations that could truly change crypto? Are they more decentralized or secure than Ethereum? The answer to both is no. They haven’t introduced any groundbreaking narratives either. All they’ve done is make those seemingly complex technologies feel more like real-world applications, blending Web2 standards with blockchain advantages, and that’s all.

As Ethereum experiences internal exponential growth while external liquidity remains scarce, the quest for new narratives can’t fill the block space on Layer 2. As the industry leader, Ethereum should first address the fragmentation and internal decay within its Layer 2 ecosystem. Especially notable is the Ethereum Foundation (EF), which I haven’t mentioned earlier. Why, despite its massive spending, has EF failed to fulfill its role? In a market where Layer 2 infrastructure is already heavily oversupplied, why does EF continue to prioritize funding infrastructure projects? Even the leaders of CEXs are humbling themselves and seeking transformation, yet EF, the organization that is supposed to accelerate the ecosystem’s growth, seems to be moving in the opposite direction.

About YBB

YBB is a web3 fund dedicating itself to identify Web3-defining projects with a vision to create a better online habitat for all internet residents. Founded by a group of blockchain believers who have been actively participated in this industry since 2013, YBB is always willing to help early-stage projects to evolve from 0 to 1.We value innovation, self-driven passion, and user-oriented products while recognizing the potential of cryptos and blockchain applications.

YBB Capital is a venture capital firm focused on blockchain and Web3 investments. The content on this website is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any security or financial product. Any investments or portfolio companies mentioned are not representative of all investments, and there is no guarantee of future results. Information on this site may include forward-looking statements and is provided "as is" without any warranties, express or implied. YBB Capital does not provide investment, legal, or tax advice. Website access is limited to jurisdictions where such access is lawful. Users are responsible for complying with applicable local regulations.